UK Dental Lab Market Enters New Era as Technology and Investment Reshape the Industry

By Ioana Nobel and Finlay Sleeman

The UK dental laboratory sector, long characterised by a highly fragmented landscape of locally focused operators, is undergoing a period of significant change. A wave of technological innovation, from digital workflows to advanced manufacturing, is accelerating transformation across the industry. Workforce shortages and market consolidation have also begun to reshape the market. These dynamics are redefining the competitive environment, making it more attractive for further private equity (PE) investment.

Digital Technologies Redefine the Lab of the Future

The industry is changing from a disconnected set of laboratories where dental technicians manufacture products by hand, to a world of digital workflows and large-scale automated production involving intra-oral scanning, 3D printing, and robotics. This enables dental labs to grow at scale, making the sector more attractive for investors and buy and build strategies.

CAD/CAM systems allow the precise design and manufacture of restorations. Digital files sent by dental practices from intraoral scans enable faster turnaround times, more precise fabrication, and enhanced collaboration with clinicians. As some dentists still work with traditional impressions, the CAD software can turn these into digital impressions. While CAD/CAM systems are not new – in 2019, 45% of small labs and 98% of large labs in the U.S and Europe had a CAD/CAM system – the technology behind them continues to improve, with EQT Partners-backed CAD supplier 3Shape recently introducing tools such as AI-powered design proposals.

Increased adoption of 3D printing enables labs to rapidly produce high-quality dental models, surgical guides, and dentures, which reduces patient wait times. In the U.S, 3D printer use in dental labs has grown from 16% in 2015 to 74% in 2025, with the UK following suit: last year, Derby-based 3D printing supplier SYS Systems announced a 350% surge in dental market sales. In reducing manual labour expenditure and supporting batch production, whilst being quicker and more precise than traditional methods, 3D printers improve margin opportunities for labs.

Artificial Intelligence (AI) is rapidly moving from being a diagnostic aid to a practical tool within the lab, automating product design, quality control, and workflow processes to increase accuracy. Dental labs in the UK are beginning to integrate AI and machine learning technologies into their digital workflows: from optimising the design of dental restorations, supporting smart materials detection, predicting restoration longevity, and identifying potential issues such as misaligned bites. For example, in recent years Voxel3Di became the first British company to develop dedicated dental AI software solutions, such as being able to almost instantly deliver online cephalometric digitisation and analysis to dental specialists.

Fragmented Market Begins to Consolidate

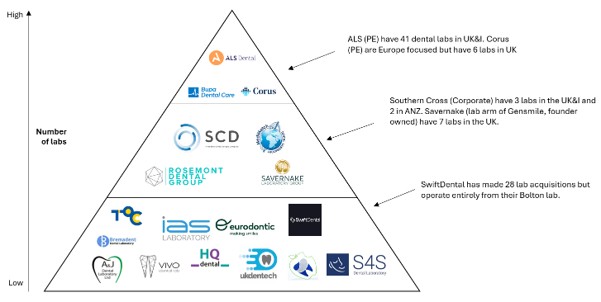

The Dental Labs Association (DLA) has over 1,000 members and accounts for 80% of national output. Luminii’s analysis shows that dental labs are quite locally dispersed, with the UK’s 10 largest metropolitan areas containing less than 30% of all UK dental labs registered with the DLA-run British Bite Mark (BBM). On the market segmentation, while there has been significant consolidation in recent years, the industry remains highly fragmented, as shown below.

Increasing PE and M&A activity

ALS Dental – created in 2019 by Ansor LLP partners Peter Strafford and Peter Marson – are the major player in the market and have acquired over 40 dental labs in the UK. Recognising the growth potential in building a large dental laboratory group, ALS has rapidly grown through serial acquisitions and organic development in the crown and bridge and orthodontic sectors, with a strong pipeline fuelling ongoing expansion.

In January 2023, the European consolidator Corus announced their entry into the UK market through the acquisition of Byrnes Dental Lab. Since then, the company has made five further UK acquisitions. Owned by Careventures PE, Corus operate more than 70 dental labs across 9 European countries and have a revenue of £180m. MediMatch are a third PE-backed player, having received investment in 2025 from Queens Park Equity. MediMatch serve more than 2,000 dentists nationally and has labs in London, Dublin, Milan, and Paris. MediMatch’s digital-first approach helped it grow at around 20% per annum in the three years prior to QPE’s investment, and it is well positioned to successfully pursue a release of equity to fund its expansion strategy of acquisitions in the UK and Europe.

There are also noteworthy providers that are not backed by PE firms. For example, the Bupa Dental conglomerate has various in-house dental labs including Synergy Ceramics in Wolverhampton and Lab 53 in London. Another is Gensmile – established in 2015 by two ex-Warburg Pincus MDs – which has acquired 41 dental practices and 5 dental labs and in 2018 set up Savernake Laboratory Group, who now operate an additional 7 dental labs in the UK. Other providers undertaking M&A include Rosemont Dental Group, which was established in 2022 and operates a partnership-based approach across its three dental labs, and Swift Dental, who have made 28 acquisitions and service 6,000 dentists from their lab in Bolton.

Investment Potential: A Sector on the Cusp of Scale

The dental lab sector appears to be primed for further investment. The UK dental lab market is currently sized at around £900 million, and Eclipse CF estimated a CAGR of 6% as it grows to a projected value of £1.3 billion by 2030. PE firms have begun to recognise this opportunity, investing in labs with buy and build strategies aimed at fostering growth, improved service offerings, and ensuring dental professionals can access cutting-edge solutions. Technological advancements and digitisation are facilitating lab decentralisation, which supports the ability of PE-backed dental labs to scale.

‘By 2030, we’ll see a massive decentralisation of lab services. Remote design teams will become common, powered by global talent and platforms that manage case flow in real time. Some labs will even go fully virtual – no physical facility, just designers, cloud-based software and manufacturing partners.’ – Corus Byrnes Dental Lab

There is still a large pool of dental labs for PE firms to consider. For example, IAS Laboratory serve hundreds of NHS and private clinics from its Surrey base and boast 10 international lab partnerships across Europe, the U.S, Australia, the UAE, and South Africa. Another promising player is UK Dentech, a digital-first dental lab based in Hampshire that specialises in digital workflows for dental restorations, crown and bridge work, implant prosthetics, and orthodontic appliances, and supports over 300 dentists.

Labour and Regulation: Growing Pains Amid Rapid Change

A potential barrier to investment is the current shortage of dental lab technicians: The General Dental Council’s figures show that dental technicians are the only category of dental professionals that experienced a decline in their labour force from 2023 to 2025. This decline is in line with the long-term trend for the profession.

'In 2008, there were 7,460 dental technicians in the UK, supporting a workforce of 36,281 dentists – a ratio of 4.86 dentists to every technician. In 2024 the numbers have further declined: 4,895 technicians to 46,362 dentists, representing a shocking ratio of 9.16 dentists for every technician.’ – Dentistry

Increased digitalisation could cushion the impact of this decline in dental technicians. However, the dental technicians of the future will need a new set of skills to enable them to work in digital labs, which labs currently struggle to recruit for. This is in part because the average dental technician in the UK is in their mid-50s. As such, programmes to support new entrants into the profession are critical. This month, a Welsh university announced a partnership to deliver a higher apprenticeship in dental technology. However, the Dental Technologists Association (DTA) remain concerned: Pearson recently withdrew the Level 3 Dental Technology Programme in Northern Ireland, and programmes across Scotland and England are at risk of closure. Moreover, from July 2025, dental technicians no longer qualify for the UK’s Skilled Worker visa. This change reflects the tightening of immigration rules and could worsen staffing shortages for dental labs.

On regulation, many industry participants are unsure as to the rules overseeing how dental labs and technicians operate. For example, in a recent survey 80% of respondents said the two main regulatory bodies for dental labs, the GDC and MHRA, do not make it clear who is permitted to sign the statement of manufacture for custom-made dental devices. Further, 20% of respondents incorrectly believed that dentists using CAD/CAM did not have to register with the MHRA. Investors should be mindful to navigate these labour force and regulatory challenges.

A Sector Poised for Transformation — With Caution

The UK dental lab industry is undeniably at a turning point. Digitalisation is improving quality, reducing production times, and enabling scale. Investors are pouring in, confident that the sector can be modernised much like dental practices were a decade ago. Yet major challenges remain: a shrinking workforce, fragile training pathways, and regulatory ambiguity. For private equity firms, success will require balancing the efficiencies of scale with the relationship‑driven culture of dentistry, where many clinics remain loyal to the single lab they’ve trusted for years. The race to modernise the dental lab is underway, and the next five years will determine who leads this new era of digital dentistry.

Bibliography

British Bite Mark (DLA). 2026. https://dentallaboratory.org.uk/

Byrne, A. 2025. “What will a dental laboratory look like in 2030?” Dentistry: https://dentistry.co.uk/2025/05/22/what-will-a-dental-laboratory-look-like-in-2030/

Dental Technologists Association. 2025. “DTA Raises Urgent Concerns Over the Future of Dental Technology Training in the UK.” DTA: https://www.dta-uk.org/news/dental-technologists-association-raises-urgent-concerns-over-the-future-of-dental-technology-training-in-the-uk-

Drevenstedt, G. 2025. “Three Out of Four Labs Now Use 3D Printers: New Results from NADL’s Dental Technology Survey.” NADL: https://res.cloudinary.com/carbon3d/image/upload/NADL_REPORT_2025.pdf

Eclipse Corporate Finance. 2024. “Dental Laboratory M&A UK Landscape.” Eclipse: https://www.eclipsecf.com/post/dental-laboratory-m-a-uk-landscape

Everatt, M. 2024. “Is this the end for dental technicians?” Dentistry: https://dentistry.co.uk/2024/08/29/is-this-the-end-for-dental-technicians/

Everatt, M. 2024. “The curious demise of dental technicians.” Dentistry: https://dentistry.co.uk/2024/01/09/the-curious-demise-of-dental-technicians/

General Dental Council. 2026. “Registration Report.” GDC: https://www.gdc-uk.org/about-us/what-we-do/the-registers/registration-reports

Nyctelius, H. 2020. “The Future of Dentistry is Digital.” Roland Berger: https://www.rolandberger.com/en/Insights/Publications/The-Future-of-Dentistry-is-Digital.html

Veal, L. 2025. “How does the profession feel about dental technology regulation?” Dentistry: https://dentistry.co.uk/2025/07/16/addressing-the-mystery-of-dental-technology-regulation/

Latest news

-

17 Jun 2026

Beyond the Megadeal: The Quiet Roll-Up Revolution in European Cybersecurity

-

20 May 2026

Luminii provides strategic & CDD support to YFM and GEEIQ’s Management team on YFM’s follow-on investment

-

17 Apr 2026

Luminii provides Commercial Due Diligence support to Palatine and Papilo on their acquisition of REKK Recycling

-

14 Apr 2026

Bridging the Mental Health Gap: How Private Equity and Venture Capital are Reshaping UK Provision

-

02 Apr 2026

Luminii provides Commercial Due Diligence to YFM on its investment in Aura