Bridging the Mental Health Gap: How Private Equity and Venture Capital are Reshaping UK Provision

By Finlay Sleeman

The UK is experiencing record highs in people reporting mental health problems whilst the sector faces a chronic labour shortage, resulting in a mental health waiting list of 1.7 million people. Since 2016, the number of children and young people in contact with mental health services has increased by over four times the rate of the psychiatry workforce, and while mental health accounts for 20% of illness the NHS has to treat, it receives less than 9% of total funding. Amidst a strained NHS, there is growing demand for specialised private mental health provision across a spectrum of services, from counselling to complex inpatient care. As demand for services across the system has risen, independent sector providers have played an increasingly important role in helping the NHS meet demand. These mental health services to the NHS range from wellness and prevention support to rehabilitation services and secure adult inpatient wards.

The NHS reliance on private sector providers, continued increases in insurance reimbursements, higher prevalence of employers offering mental health support funding, and the greater willingness of individuals to privately fund treatment have fuelled demand for private mental health services, making it an attractive investment for private equity.

Given this, as well as increased government funding for mental health support, investors are beginning to look at technology-first businesses that streamline operations and offer education and treatment. In the last two years, UK investment firms such as RYSE Asset Management and Spex Capital respectively have launched $50m and $100m funds dedicated to digital mental health and med-tech start-ups. In 2025, London-based Cera reached over £400m in raised capital following investment from BDT & MSD Partners and Schroders Capital, aimed at scaling its AI-led healthcare technology. With strong tailwinds and an array of founder-led businesses, the sector is primed for further PE and VC investment.

A Growing Market Opportunity

As the chart below shows, NHS spend on mental health has been growing year on year and is projected to increase by 10.8% in 2025/26, to reach over £20 billion. While the NHS still dominates, private providers are growing, supported by NHS outsourcing and the Right to Choose initiative. Indeed, a 2025 King’s Fund study found that the share of NHS mental health inpatient care being outsourced to independent providers has increased significantly, with 29% of NHS-funded mental health bed capacity being provided by the private sector.

There are also a large proportion of businesses offering mental health support for employees, which often go through private mental health service providers. Indeed, a 2025 survey of 500 HR leaders found that 54% of UK employers offer mental health support, rising to 78% for businesses with over 250 employees. Broadstone, an employee benefits consultancy, reported a sharp increase in mental health claims made by employees, from 8% in 2022 to 13% in 2025.

Given the significance of the public sector, government policy is a key market dynamic. Across healthcare, the UK government has pushed for increased digitisation, demonstrated by the continued target for 80% of healthcare providers to adopt Digital Social Care Records, and that digital transformation is one of three fundamental shifts outlined in the 2025 NHS 10 Year Health Plan for England.

For mental health in particular, around a third of NHS mental health treatments are already online, with digital mental health therapy estimated to save 6,000 therapist hours per 1,000 patients. On the workforce – due to chronic labour shortages – the recent NHS Long Term Workforce Plan aims to increase training places for mental health nursing by 93% by 2031/32. On investment, Innovate UK has a £20m budget to invest in start-ups within the UK’s immersive digital mental health sector, while British Patient Capital operates a £425m fund for growth stage, R&D-intensive companies in Life Sciences and Deeptech. Given the need for investment, PE and VC firms should benefit from a supportive policy environment when investing in the mental health technology space.

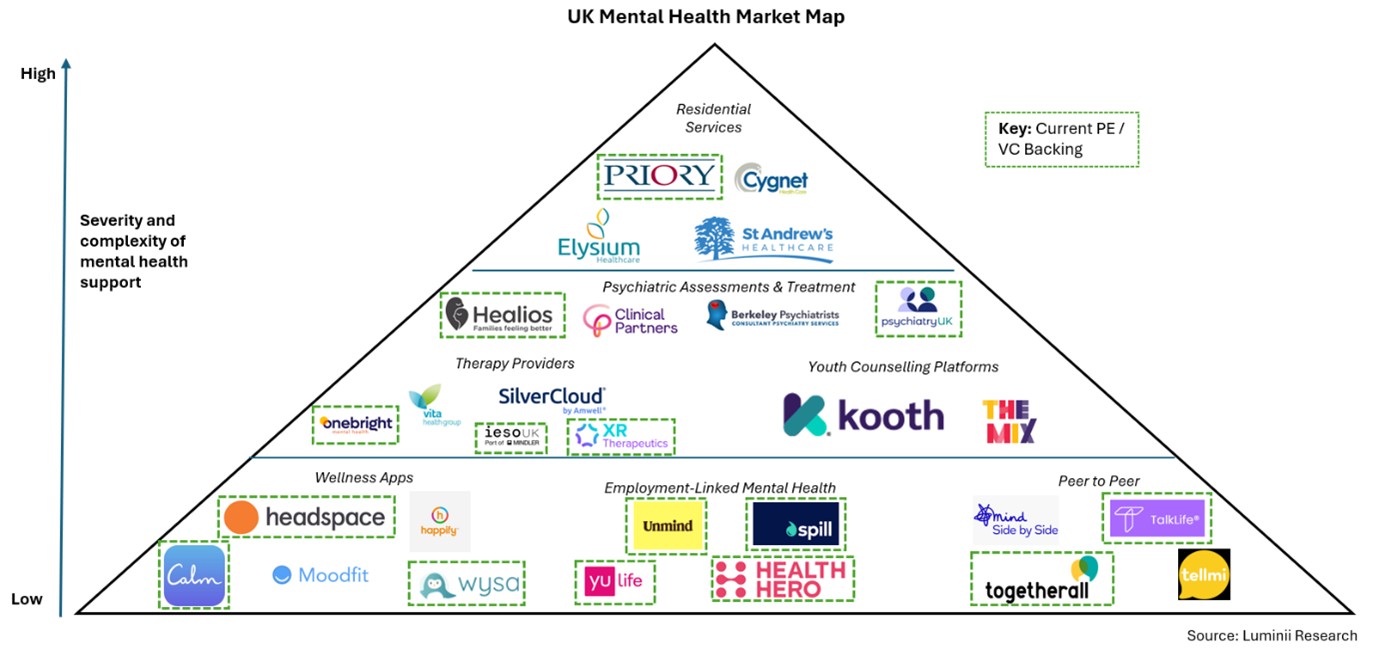

Fragmentation Leaves Room for Consolidation

The UK market can first be split between the providers of residential mental health services and digital providers. Within the digital mental health market there is further segmentation, such as between immersive technology providers, wellbeing apps, operational software, and online therapy: different provision is required for differing severity of mental health difficulties. The market map below shows this for the UK.

The market exhibits a long tail, with a few well-established providers and a large number of small start-ups. For traditional, residential mental health provision there is strong market concentration, with the four largest providers, Cygnet Heath Care, The Priory Group, Elysium Healthcare, and St Andrew’s Healthcare (a charity), estimated to comprise 68% of the market. However, the emerging digital market is far less concentrated. According to Beauhurst, there are an estimated 5,898 mental health-focused companies in the UK, with 31.3% in psychiatry, psychotherapy, and counselling and 25% in application software. There are also over 20,000 mental health apps available in the UK. Further, in a recent University of Liverpool study on the UK’s XR mental health landscape, 78% of private sector respondents were micro companies.

The heavily concentrated residential mental healthcare market saw substantial M&A activity in the 2010s. For example, The Priory Group – backed by Waterland PE – acquired Castlecare in 2014 and Progress Care and Life Works in 2015, Cygnet brought Alpha Hospitals (2015) and Cambian’s adult services division (2016), while Elysium Healthcare acquired Ralphael Healthcare and Lighthouse Healthcare in 2017 and 2018. As such, between 2015 and 2019 the traditional market concentration, measured by the four dominant non-NHS providers’ proportion of mental health hospital beds, rose from 52% to 64%. However, the digital mental health market has not witnessed anything like this level of M&A, leaving the opportunity open for investors.

Recent Investment Trends

The UK mental health market continues to attract PE investment, albeit activity levels are uneven across sub-sectors. Businesses that are able to demonstrate scale and credible routes to a mix of funding channels (such as the NHS, DfE, employer, insurance, and direct-to-consumer) are likely to continue to attract investors’ attention.

Beauhurst’s data states UK mental health-focused companies have raised £1.86b in equity in UK since 2011. This peaked at £448 million in 2021, and there has been £215m raised from January to November 2025. This includes notable investment in traditional mental health service providers, such as The Priory Group (Waterland PE), Active Care Group (Montreux Healthcare Fund), and Vita Health Group (Archimed PE). However, there has also been a recent uptick in investment aimed at predominantly digital providers. For example, in 2024 Queens Park Equity acquired Psychiatry UK and YFM Equity acquired Psychology Tools, both of which are digital players. The table below outlines recent PE and VC investment in UK headquartered, technology-focused mental health companies.

Conclusion

Technology used for mental health services presents an interesting and growing market opportunity for investors as there is continued government funding, a severe public sector gap in supply and demand, and a much lower market concentration than for traditional, residential mental health support. The market has seen an increase in PE and VC investment in recent years, with this trend likely to continue.

Sources

BMA, 2025

NHS, 2025

theHRDirector, 2025

Gov.UK, 2025

The Guardian, 2023

National Health Executive, 2024

NHS England, 2023

Cooper Parry, 2025

Innovate UK, 2025

Beauhurst, 2025

UK Parliament, 2025

Mansfield Advisors, 2022

King’s Fund, 2025

Latest news

-

27 Jul 2026

Luminii provides Commercial Due Diligence support to Ideagen on their acquisition of Work Wallet

-

17 Jun 2026

Beyond the Megadeal: The Quiet Roll-Up Revolution in European Cybersecurity

-

20 May 2026

Luminii provides strategic & CDD support to YFM and GEEIQ’s Management team on YFM’s follow-on investment

-

17 Apr 2026

Luminii provides Commercial Due Diligence support to Palatine and Papilo on their acquisition of REKK Recycling

-

14 Apr 2026

Bridging the Mental Health Gap: How Private Equity and Venture Capital are Reshaping UK Provision